The Minimum Necessary Income (or “MNI”) requirement affects the ability of a Canadian citizen or permanent resident to sponsor certain foreign national members of the family class.

IRPR s. 120 states (emphasis added):

120. For the purposes of Part 5,

(a) permanent resident visa shall not be issued to a foreign national who makes an application as a member of the family class or to their accompanying family members unless a sponsorship undertaking in respect of the foreign national and those family members is in effect; and

(b) a foreign national who makes an application as a member of the family class and their accompanying family members shall not become permanent residents unless a sponsorship undertaking in respect of the foreign national and those family members is in effect and the sponsor who gave that undertaking still meets the requirements of section 133 and, if applicable, section 137.

Section 133(1)(j) states (emphasis added):

133. (1) A sponsorship application shall only be approved by an officer if, on the day on which the application was filed and from that day until the day a decision is made with respect to the application, there is evidence that the sponsor…

j) if the sponsor resides

(i) in a province other than a province referred to in paragraph 131(b),

(A) has a total income that is at least equal to the minimum necessary income, if the sponsorship application was filed in respect of a foreign national other than a foreign national referred to in clause (B), or

(B) has a total income that is at least equal to the minimum necessary income, plus 30%, for each of the three consecutive taxation years immediately preceding the date of filing of the sponsorship application, if the sponsorship application was filed in respect of a foreign national who is

(I) the sponsor’s mother or father, (my note: i.e. parent)

(II) the mother or father of the sponsor’s mother or father, (my note: i.e. grandparent) or

(III) an accompanying family member of the foreign national described in subclause (I) or (II), and

(ii) in a province referred to in paragraph 131(b), is able, within the meaning of the laws of that province and as determined by the competent authority of that province, to fulfil the undertaking referred to in that paragraph;

“Minimum necessary income” is defined in IRPR sections 2 and 134 and identified as “… the minimum amount of before-tax annual income necessary to support a group of persons ….”

minimum necessary income means the amount identified, in the most recent edition of the publication concerning low income cut-offs that is published annually by Statistics Canada under the Statistics Act, for urban areas of residence of 500,000 persons or more as the minimum amount of before-tax annual income necessary to support a group of persons equal in number to the total number of the following persons:

(b) the sponsored foreign national, and their family members, whether they are accompanying the foreign national or not, and

(c) every other person, and their family members,

(i) in respect of whom the sponsor has given or co-signed an undertaking that is still in effect, and

(ii) in respect of whom the sponsor’s spouse or common-law partner has given or co-signed an undertaking that is still in effect, if the sponsor’s spouse or common-law partner has co-signed with the sponsor the undertaking in respect of the foreign national referred to in paragraph (b). (revenu vital minimum)

By the above definition, it is important to properly calculate the size of your family and as well take into account any changes that might occur if your family size were to change during the application process.

It is also important to note R.134(1) on how income is calculated, especially the exclusions and how that may affect the income amounts (emphasis added)::

Income calculation rules

134 (1) Subject to subsection (3), for the purpose of clause 133(1)(j)(i)(A), the sponsor’s total income shall be calculated in accordance with the following rules:

(a) the sponsor’s income shall be calculated on the basis of the last notice of assessment, or an equivalent document, issued by the Minister of National Revenue in respect of the most recent taxation year preceding the date of filing of the sponsorship application;

(b) if the sponsor produces a document referred to in paragraph (a), the sponsor’s income is the income earned as reported in that document less the amounts referred to in subparagraphs (c)(i) to (v);

(c) if the sponsor does not produce a document referred to in paragraph (a), or if the sponsor’s income as calculated under paragraph (b) is less than their minimum necessary income, the sponsor’s Canadian income for the 12-month period preceding the date of filing of the sponsorship application is the income earned by the sponsor not including

(i) any provincial allowance received by the sponsor for a program of instruction or training,

(ii) any social assistance received by the sponsor from a province,

(iii) any financial assistance received by the sponsor from the Government of Canada under a resettlement assistance program,

(iv) any amounts paid to the sponsor under the Employment Insurance Act, other than special benefits,

(v) any monthly guaranteed income supplement paid to the sponsor under the Old Age Security Act, and

(vi) any Canada child benefit paid to the sponsor under the Income Tax Act; and

(d) if there is a co-signer, the income of the co-signer, as calculated in accordance with paragraphs (a) to (c), with any modifications that the circumstances require, shall be included in the calculation of the sponsor’s income.

Exception

(1.1) Subject to subsection (3), for the purpose of clause 133(1)(j)(i)(B), the sponsor’s total income shall be calculated in accordance with the following rules:

(a) the sponsor’s income shall be calculated on the basis of the income earned as reported in the notices of assessment, or an equivalent document, issued by the Minister of National Revenue in respect of each of the three consecutive taxation years immediately preceding the date of filing of the sponsorship application;

(b) the sponsor’s income is the income earned as reported in the documents referred to in paragraph (a), not including

(i) any provincial allowance received by the sponsor for a program of instruction or training,

(ii) any social assistance received by the sponsor from a province,

(iii) any financial assistance received by the sponsor from the Government of Canada under a resettlement assistance program,

(iv) any amounts paid to the sponsor under the Employment Insurance Act, other than special benefits,

(v) any monthly guaranteed income supplement paid to the sponsor under the Old Age Security Act, and

(vi) any Canada child benefit paid to the sponsor under the Income Tax Act; and

(c) if there is a co-signer, the income of the co-signer, as calculated in accordance with paragraphs (a) and (b), with any modifications that the circumstances require, shall be included in the calculation of the sponsor’s income.

Finally, a clause that frequently captures individuals, especially in those applications that take increased time to process is IRCC’s ability under R. 134(2) [subject to R.134(3) calculation rules] to ask for updated evidence of income if more than 12 months have elapsed since the receipt of the sponsorship application or an officer receives information that the sponsor is no longer able to fulfil the obligations of the sponsorship undertaking (emphasis added):

Updated evidence of income

(2) An officer may request from the sponsor, after the receipt of the sponsorship application but before a decision is made on an application for permanent residence, updated evidence of income if

Modified income calculation rules

(3) When an officer receives the updated evidence of income requested under subsection (2), the sponsor’s total income shall be calculated in accordance with subsection (1) or (1.1), as applicable, except that

(a) in the case of paragraph (1)(a), the sponsor’s income shall be calculated on the basis of the last notice of assessment, or an equivalent document, issued by the Minister of National Revenue in respect of the most recent taxation year preceding the day on which the officer receives the updated evidence;

(b) in the case of paragraph (1)(c), the sponsor’s income is the sponsor’s Canadian income earned during the 12-month period preceding the day on which the officer receives the updated evidence; and

(c) in the case of paragraph (1.1)(a), the sponsor’s income shall be calculated on the basis of the income earned as reported in the notices of assessment, or an equivalent document, issued by the Minister of National Revenue in respect of each of the three consecutive taxation years immediately preceding the day on which the officer receives the updated evidence.

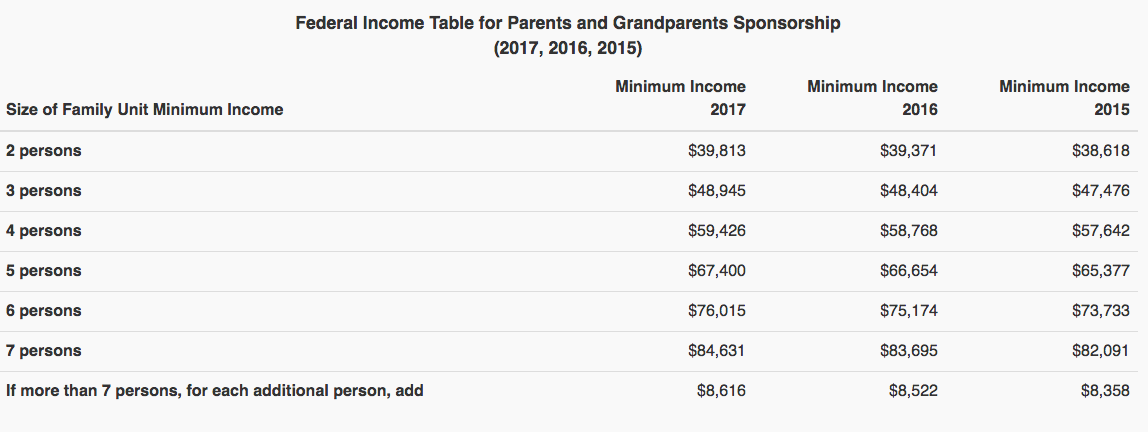

What is the $$ Required for the Minimum Income Requirement (as of the date of this post)?

IRCC sets out the MNIs for parent and grandparent sponsorship, which discussed above, are the Minimum Necessary Income (“MNI”) plus 30%. IRCC obtains that information by either by an Applicant’s consent on Question 8 of the Financial Evaluation for Parents and Grandparents Sponsorship form or by completing the Income Sources for the Sponsorship of Parents and Grandparents form and submitting NOAs for the three preceding years.

Expect this to change with the 2019 program reveal (requiring 2018, 2017, and 2016 Minimum Income)

Co-Signer

A co-signer’s undertaking is governed by R. 132(5) IRPR which draws the minimum income requirement provisions of R. 133(1) and R. 134 into the fold.

Co-signature — undertaking

(5) Subject to paragraph 137(c), the sponsor’s undertaking may be co-signed by the spouse or common-law partner of the sponsor if the spouse or common-law partner meets the requirements set out in subsection 130(1), except paragraph 130(1)(c), and those set out in subsection 133(1), except paragraph 133(1)(a), and, in that case,

(a) the sponsor’s income shall be calculated in accordance with paragraph 134(1)(b) or (c) or (1.1)(b), as applicable; and

(b) the co-signing spouse or common-law partner is jointly and severally or solidarily bound with the sponsor to perform the obligations in the undertaking and is jointly and severally or solidarily liable with the sponsor for any breach of those obligations.

The above provision on the face is actually a bit confusing. The spouse needs to be meet the requirements of 130(1) except R. 130(1)(c) yet is exempted from R. 133(1)(a) , which circularly requires that the sponsor must continue to meet the sponsorship requirements from the day the application is filed until the day a decision is made.

What I interpret this to mean – although I may be wrong, so take this with a grain of salt – is that the Co-signer must meet the R. 130(1) requirements at the time the application is submitted but is not required to provide evidence of ongoing compliance. In that sense, a Co-signer could reside in another country (for example to work abroad) but the Sponsor could not (per R.130(1)(b) and R. 133(1)(a) IRPR).

Co-signer issues can be quite complicated (especially with updating relationships)- I won’t go into too many details in this post but see Agyemang v Canada (Citizenship and Immigration), 2018 CanLII 115279 (CA IRB) for a representative case of the complexities that may occur.

IRCC sets out the requirements for a co-signer in their policy guide as follows:

May I have a co-signer?

Your spouse or common-law partner may help you meet the income requirement by co-signing the sponsorship application. A common-law partner is a person who is living with you in a conjugal relationship and has done so for at least one year prior to the signing of the undertaking.

The co-signer must:

- meet the same eligibility requirements as the sponsor;

- agree to co-sign the undertaking;

- agree to be responsible for the basic requirements of the person you want to sponsor and his or her family members for the validity period of the undertaking.

The co-signer will be equally liable if obligations are not performed.

If your co-signer is a common-law partner, you must submit the Statutory Declaration of Common-Law Union (IMM 5409).

One of the current major gaps is that IRPR does not allow siblings (such as brothers/sisters) to both serve as co-signers. I would suggest that in many cases, allowing this type of arrangement (or at least some public policy exemption) may make more sense than having an in-law serve in that role.

Why are the MNIs so contentious – Some Case Law and Experiences

2014 Change in Regulations

In 2 January 2014, IRPR ss. 133(1)(j) and s. 134 was amended to increase the MNI by 30 percent for this appeal from that considered by the visa officer. Madam Justice Simpson in Tharmarasa v. Canada (Citizenship and Immigration), 2018 FC 1174 (CanLII) examined the Regulatory Impact Analysis Statement [RIAS], finding that the IAD should have applied the old regulations, departing from the approach taken by the Federal Court in Patel v. Canada (MCI) 2016 FC 1221 and Begun v. Canada (MCI) 2017 FC 409.

Still other members have taken a different approach. In X (Re), 2018 CanLII 101225 (CA IRB)

[9] Section 133(1)(j)(i)(B) of the Regulations applies to the Appellant’s sponsorship application because she is sponsoring a parent. On January 1, 2014, section 133(1)(j)(i) of the Regulations was amended to increase the MNI by thirty percent for the sponsorships of parents. Section 134 (1.1) of the Regulations also provides the income calculation rules that are applicable in cases where an appellant sponsors their parents. Prior to 2014, the calculation required assessing the income an appellant earned in the year immediately preceding the sponsorship application. Since January 1, 2014, the calculation requires assessing income earned in each of the three consecutive taxation years immediately preceding the date of the filing of the sponsorship application.[3]

[10] In Gill,[4] it was held that the sponsor did not have the right to have her application determined under the previous version of the Regulations, as people who apply for permanent residence have no accrued or accruing rights until a final decision has been made on their application. The final decision on an application is the Immigration Appeal Division (IAD) decision. Therefore, the sponsorship requirements applicable at the time of this appeal are the requirements under the amended Regulations. This sponsorship application for the Appellant’s father was filed on June 28, 2010. Despite Gill, the parties at the hearing agreed that they would consider the visa officer’s assessment of the Appellant’s income for 2014 only. The parties agreed that the MNI had not been met for ten persons at the time of the assessment. [5]

[11] As such, I find that the visa officer’s refusal is legally valid.

It is not uncommon for two lines of jurisprudence to come out of the Federal Court – an issue I hope IRCC will try to navigate by clarifying instructions to IAD board members.

There also are implications for the new thresholds in appeals. As the Panel in Rajah v Canada (Citizenship and Immigration), 2018 CanLII 107684 (CA IRB) sets out – the present ability to meet the new MNIs may lower the threshold re: discretionary relief.

Discretionary Relief – Is the Lower Threshold Available?

[14] For the purpose of determining the standard of discretionary relief to be applied in a financial refusal, the sponsor’s ability to meet the MNI at the date of hearing is relevant. The cases of Jugpall[9] and Dang[10] suggest that a lesser standard of granting relief will be applicable in cases where the appellant now meets the financial requirements of sponsorship.

[15] As I have previously held, it is my view that the current MNI provisions for sponsoring parents should apply when determining if a sponsor now meets the financial requirements under the IRPA and its Regulations.[11] Chief Justice Crampton’s decision in Gill[12] confirms that the new MNI requirements should apply when determining if an appellant is to have access to a lower threshold for the exercise of special relief. The issue was also more recently considered by Justice Russell in Sran,[13] where the Court determined that the IAD’s use of the new regulatory provision in this context was reasonable. As such, the onus is on the appellant to establish based on Revenue Canada Notices of Assessment that he met the MNI for the past three years.

[16] In her written submissions, counsel for the appellant concedes that the appellant did not meet the MNI for 2015 and 2016. The lower Jugpall threshold does not apply.

In this matter, the Appellant was ultimately successful in demonstrating humanitarian and compassionate grounds and the appeal was allowed.

IRCC Incorrectly Relying on Tax Years Four Years Back – the Shifting Window/Alternative Forms of Income

One of the historical issues that made assessment very challenging was IRCC’s practices of ‘skipping’ the most immediate year due to the fact taxes were not filed by the time the Application to Sponsor went in.

Still, the shifting window or even the “uncertainty” of whether one meets the tax requirements of a particular filing years. Certain times, especially where individuals are self-employed, there will be conflict between the amount that it makes sense to declare for tax and what is best for the business.

Calculating Family Size

The issues of calculating family size were also prominent in X (Re) 2018. From paragraphs 18-31, the Member had to assess whether certain half-siblings were dependent who were 21 and just under the age where a child stops becoming dependent were being cared for by the Sponsor.

In cases such as as Alavehzadeh v Canada (Citizenship and Immigration), 2016 CanLII 73710 (CA IRB) [and the companion case Begum v Canada (Citizenship and Immigration), 2016 CanLII 73712 (CA IRB), that eventually went up to the FC and FCA] IAD Panels have faced situations, when assessing humanitarian and compassionate considerations, from applicants who come from large multi-family units, where siblings work to contribute to the household and an Appellant themselves may not have the funds themselves. In Alavehzadeh, the Panel found that s.67 allowed for considerations that may overcome deficiency and provides sufficient broad discretion to take into account individual circumstances.

We saw this in Jir v Canada (Citizenship and Immigration), 2018 CanLII 81824 (CA IRB), where the Sponsor’s consistent work history and cash-only payment as a babysitter contributed to a positive humanitarian and compassionate grounds finding, even though there was a lack of proof of the payment.

Unfortunately, the Federal Court of Appeal in Begum ruled decisively that MNIs do not violation s.7 and s.15 of the Charter, finding there was no Charter right to family reunification (see Begum v. MCI 2018 FCA 181 at paras 100-110) and that there quantitative evidence fell short of meeting the burden of demonstrating an adverse impact (see Begum v. MCI 2018 FCA 181 at paras 41-92).

Updating the Visa Office Diligently

It is very important to ensure that visa offices are updated as soon as changes occur and that any implications on the MNI are brought to the Officer’s attention. I have been involved in several cases where visa officer’s mistakenly consider a newborn child as part of the MNI in a tax-year where they have not yet been born. these changes are not always intuitive and the relevant tax years (as we discussed above) is often a source of internal confusion.

Hope this posts helps you navigate the MNI! I eagerly await seeing how the 2019 process will work out 🙂